In October 2022, Kroger and Albertsons announced plans to merge in a deal worth .6 billion. Kroger is the fourth-largest grocery retailer in the U.S., while Albertsons is fifth. Combined, they will still be far behind market leader Walmart. Kroger operates 2,726 stores under various names, and Albertsons has 2,278 stores. In comparison, Walmart and Sam’s Club have over 5,300 stores, with grocery sales more than double those of Kroger and Albertsons combined.

This significant merger would only give the combined company about 9% of national grocery sales. However, their market share would be far higher in some areas, raising concerns about reduced competition and more control over the workforce and suppliers. Kroger and Albertsons plan to sell 413 stores and eight distribution centers to C&S Wholesale Grocers for $1.9 billion to address these concerns.

Analyzing Kroger Company

Given that the Kroger Company holds the dominating position in the food retail market in the US, compared to Albertsons Companies, it has shown a great distance with the leader, Kroger, coming nearly two times larger in terms of sales. The company had its humble beginnings in its signature grocery store, which was founded in Cincinnati, Ohio, in 1883.

Today, it boasts a broad range of retail shops, which include supermarkets and fuel centers, among others. The ranges are the most popular categories within the market. The company’s products have seen an increase in growth. While Kroger has experienced a dynamic transformation into a company that holds the second place worldwide in the hypermarkets, it has persisted in being limited geographically, reaching its highest market share only within the boundaries of its own country since it generates 100% of the revenue in its home country.

Statistics & Facts About Kroger Company

The fact that Kroger runs its business in 36 states in the USA. For that, it has more than 2,700 locations, including different brands such as Fred Meyer, Ralphs, Food 4 Less, and Kwik Shop, and others. In the previous 3 years, Kroger has demonstrated stunning sales progress as its product revenue of 148 billion dollars in the year 2022, plus an increment of nearly 8% throughout the years, was almost close to 134 billion dollars in the year 2021. In 2026, it is expected, that Kroger will continue to be the foremost grocery retailer on the US market, as most of its revenue was from the supermarkets. The two categories of non-perishable goods and perishable goods yielded the most profit in the amount of approximately 74 and 35 billion respectively, with fuel sales as the third, grossing almost 19 billion, but happened to be so much more volatile than the other categories. Hardly e-commerce branches together has shown a rapid increase in sales confidence and is likely to be a substantial source of profits in the years ahead.

The U. S. Grocery, one of the most competitive markets, would require a new strategic measure.

Except the United States, grocery stores and hypermarkets typically mark a highly intricate domestic scene populated with many brands that are household names on a global basis. With the data from 2022 showing that Walmart was still the dominant food and grocery retailer with a significant margin ahead of the equally far-off third – Kroger, this new retailer managed to reach sales figures half of those reached by Walmart and behind competitors such as Amazon and Costco. Diversified portfolios of Kroger made the company’s category very specific and made it not only with similar supermarkets but with large companies that cover fuel and other kinds of trading. The most revenue-generating business of the Kroger Company was its traditional retail brand, Kroger however, the Group had opened others under Fred Meyer, Fry’s Food & Drug, and Smith’s brands as well.

Kroger’s Gross Profit History and Growth Rate (2010-2024)

Quarterly Gross Profit: January 31, 2024: Kroger’s quarterly gross profit was $8.421 billion, showing an 11.15% increase compared to last year.

Annual Gross Profit: January 31, 2024: Kroger’s annual gross profit for the twelve months ending January 31, 2024, stood at $33.364 billion, reflecting a 4.99% increase year over year.

Annual Comparison: Kroger’s annual gross profit of $33.364 billion in 2024 represents a 4.99% increase from the previous year, 2023.

Growth Rate Analysis:

- Quarterly Growth: Kroger experienced a robust 11.15% increase in quarterly gross profit compared to the previous year, indicating strong performance in the most recent quarter.

- Annual Growth: Kroger’s annual gross profit growth rate of 4.99% signifies steady expansion in profitability over the twelve months ending January 31, 2024.

- Long-Term Trends: To understand Kroger’s overall trajectory, it would be beneficial to analyze its gross profit history over the past decade, from 2010 to 2024, to identify any long-term patterns or trends in its profitability.

Kroger’s Revenue Growth (January 31, 2024)

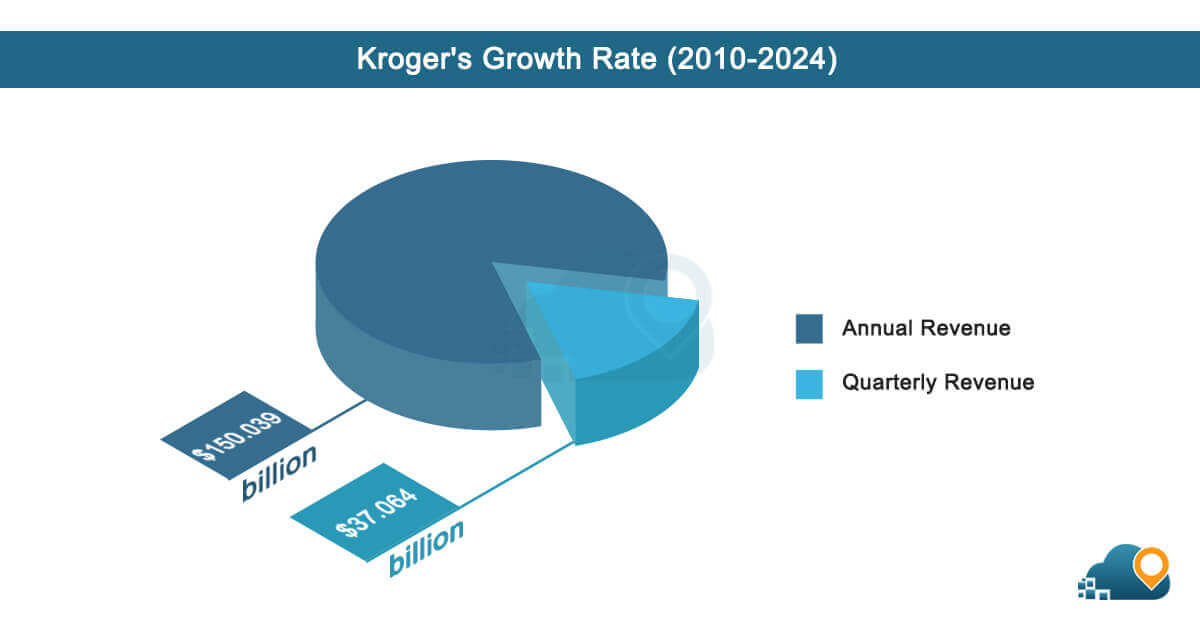

- Quarterly Revenue (January 31, 2024): Kroger’s revenue for the quarter ending January 31, 2024, was $37.064 billion, showing a 6.44% increase compared to last year.

- Annual Revenue (January 31, 2024): Kroger’s revenue for the twelve months ending January 31, 2024, totaled $150.039 billion, a 1.2% increase year over year.

- Annual Comparison (2024 vs. 2023): Kroger’s total yearly revenue was $150.039 billion in 2024, representing a 1.2% increase from the previous year, 2023.

Analyzing About Albertsons

Supermarket chains of Albertsons companies like Albertsons and Safeway have been attracting more and more consumers since 2023. They are popular within the western section of the US. However, they do have stores of a relatively smaller size in other regions of the United States, such as in the mid-western, southern, northeastern, and mid-Atlantic regions. It is because this organization operates different kinds of stores, means it gets shoppers from many dissimilar areas.

Key Facts About Albertsons

Albertsons currently operates 378 outlets and is located in 15 states and territories across the United States. These stores are established in 227 cities, which proves the versatility of the chain belonging to Albertsons. Organizing such a geographic spread enables the firm, Albertsons, to reach a broad clientele nationwide.

Most Albertsons stores are located in California, with 124 stores making up about 33% of their total locations. This means there is one Albertsons store for every 318,645 people in the state. Texas and Idaho also have a significant number of Albertsons stores. Texas has 43 stores, about 11% of the total, with one store for every 674,326 people. Idaho has 37 stores, making up about 10% of the total, with one store for every 48,297 people.

Highlights:

Albertsons Companies, Inc. (NYSE: ACI) has released its financial results for the fourth quarter and full year of fiscal 2023, ending on February 24, 2024. In the fourth quarter, identical sales increased by 1.0%, digital sales jumped by 24%, and loyalty members grew by 16% to 39.8 million. The company reported a net income of $251 million, or $0.43 per share, and an adjusted net income of $318 million, or $0.54 per share, with an adjusted EBITDA of $916 million. For the full fiscal year, identical sales went up by 3.0% and digital sales by 22%, with a net income of $1,296 million, or $2.23 per share, and an adjusted net income of $1,694 million, or $2.88 per share, and an adjusted EBITDA of $4,318 million.

Financial Growth of Albertsons

Net sales and other revenue remained steady at $18.3 billion compared to the same period last year. The primary driving factors saw 1.0% increase in identical sales, which boosted revenue, despite lower fuel sales and wholesale revenue. Growth in pharmacy sales and a 24% increase in the digital business contributed positively. The gross margin rate increased slightly to 28.0% from 27.8% the previous year.

However, excluding certain factors, it decreased marginally due to various operational costs, which were offset by productivity improvements and targeted price investments for customers. Selling and administrative expenses decreased slightly to 25.7% of revenue, but when specific impacts were excluded, expenditures increased due to digital development, ongoing merger costs, and other operational expenses. Other financial metrics showed a net loss on property dispositions and impairment losses of $0.8 million, compared to a gain of $61.4 million last year. Interest expense increased to $109.0 million due to lower interest income, and other expenses netted $2.4 million compared to $9.5 million of other income last year. The income tax expense was $64.3 million with an effective tax rate of 20.4%, higher than last year due to changes in federal tax laws. Net income was $250.5 million, or $0.43 per share, lower than the $311.1 million, or $0.54 per share, in the previous year. Adjusted net income was $318.0 million or $0.54 per share, compared to $459.7 million or $0.79 per share last year (excluding a tax benefit). Adjusted EBITDA was $915.8 million, down from $1,050.2 million last year. In summary, while sales remained stable, various operational factors affected profitability, resulting in lower net income and adjusted EBITDA compared to the previous year.

Quick Comparison between Albertsons and Kroger

When choosing between Kroger and Albertsons, customers usually look at things like prices, the variety of products, and how many stores are nearby. When compared to Albertsons, the huge and well-known supermarket company Kroger provides more items at lower rates. In fact, Kroger can be 11% to 56% cheaper, which is important for shoppers who want to save money.

Albertsons, while it might have higher prices and fewer products, is known for having less product recalls. This means that they pay priority to quality, which some consumers prefer than the hefty price tag that comes along with production. The number of stores that are owned both by Kroger and Albertsons is relatively similar; however, Kroger has more stores in different states, which makes it easier for people to access its services in comparison to Albertsons. For instance, with rumors of a shopping merger between these two big grocery chains, customers want to know whether it will affect the number of stores and, more so, the price of groceries.

Market Share and Growth

Kroger, with its large number of stores, already has a large share of the US grocery market. If it merges with Albertsons, it could become even bigger and significantly change the market. Then, this merger might serve to increase Kroger even further as well as consolidate its dominance in the grocery sector.

Store Experience and Customer Satisfaction

The aisles of Kroger Company stores are wide and well-paved, making it simple for consumers to get the items they want. As it pertains to store appearance, Albertsons also provides a clean, friendly environment, but some might find that the store layout is a bit challenging to navigate compared to Kroger.

Relative to its customers, Kroger generally boasts of a well devised and friendly service since the firm has taken time to train and offer good benefits to its employees. This leads to high customer satisfaction as indicated in the previous sections and as presented in the following figures. It also revealed that it has now enhanced many of its elements and customer service which demonstrate a strong desire to make the shopping experience better for Albertsons.

Private Label Product Offerings

Kroger:

Known for offering a large selection of high-quality store-brand products in many categories. These products are usually priced affordably, giving shoppers good value.

Albertsons:

Provides a diverse range of store-brand products with a focus on quality. Has worked to improve its store-brand line to compete better with national brands

Promotional Deals and Loyalty Programs

Kroger

Loyalty Program: Kroger has a loyalty program where customers earn points that can be used for discounts on gas and groceries.

Promotional Deals: They offer weekly ads with various discounts and digital coupons available through their app or website.

Albertsons

Loyalty Program: Albertsons has the “Just for U” rewards program, which offers personalized deals based on your shopping habits, including digital coupons and reward points.

Promotional Deals: Like Kroger, Albertsons has weekly ads with savings on specific items and sometimes offers “Buy One, Get One Free” deals on certain products.

Which Location Data Used to Compare Grocery Chains?

This analysis only includes grocery store locations on the US mainland, excluding Hawaii, Alaska, and US territories.

For Albertsons, the brands included are:

Albertsons has several different brands under its umbrella, and you might have shopped at some without even realizing they’re part of the same company. They’ve got well-known names like Safeway, Vons, and Jewel-Osco, but also others like Tom Thumb, Carrs, and Acme Markets. In total, they’ve got around 20 brands across the US, each catering to different regions and preferences.

So, whether you’re in the West and grabbing groceries at Safeway or Vons or in the Midwest popping into Albertsons or Tom Thumb, you’re likely shopping with Albertsons Companies, even if the store sign says something different. They’ve got a wide range of brands to serve many other communities.

For Kroger, the brands included are:

Kroger is another large enterprise with many subbrands or subsidiary companies. Depending on the context, some readers may know it by its previous names – Ralphs, Fred Meyer, Fry’s, and other names. And they have even more like Dillons, QFC, and other names like Harris. In total, Kroger has approximately 20 divisions across the United States and offers grocery and other services for specific communities.

Whether you purchase something from a Kroger supermarket chain, select groceries from Ralphs in California, or buy something from Fred Meyer in the Pacific Northwest, you are, in fact, helping Kroger, although it has a distinct brand name. Due to its vast coverage, Kroger has a myriad of brands in store to suit the needs of customers across the regions.

How Does Location Influence the Effects of the Grocery Chain Merger?

Understanding the Spread and Impact of the Albertsons-Kroger Merger

Creating a heat map is very helpful for visualizing where Albertsons and Kroger stores are located. This map shows where brands overlap in cities like Seattle, Los Angeles, Denver, Dallas, Chicago, and Washington DC. In these cities, stores that used to compete with each other will now be owned by the same company. If all the stores stay open after the merger, Albertsons-Kroger’s market share in these areas will increase, making it harder for smaller grocery stores to compete. However, regulators might require Albertsons-Kroger to sell or close some stores to avoid monopolies. If this happens, stores in the overlapping areas are more likely to be sold or closed.

Albertsons has more stores in the Northwestern and Northeastern U.S., while Kroger is more dominant in the Southeastern U.S., where Albertsons has no presence. If the day-to-day operations of the stores don’t change, the market share in these non-overlapping areas might stay the same. But, with the merger, Albertsons-Kroger could invest more in these stores, potentially increasing their market share even in regions without overlap.

How People Will Be Affected by the Grocery Chain Merger?

To understand how many people will be affected by the Albertsons and Kroger merger, we can look at how close people live to these stores. Using data from the 2020 U.S. Census, we estimate the number of people living within a 5-mile radius of all Albertsons and Kroger stores:

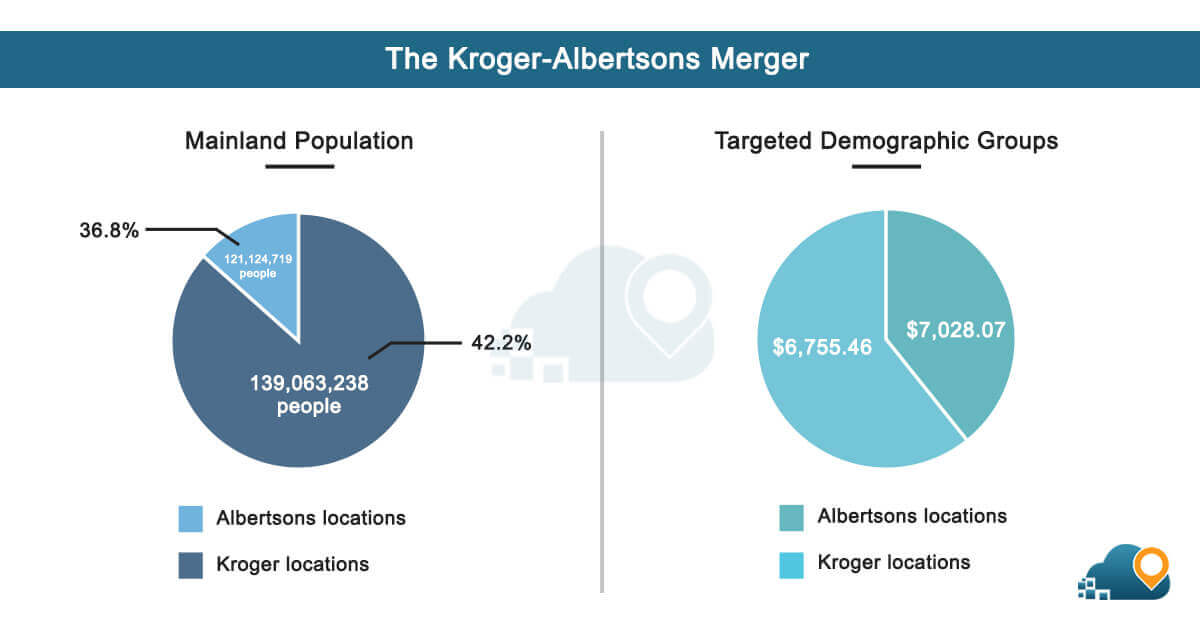

Albertsons locations: 121,124,719 people (36.8% of the U.S. mainland population)

Kroger locations: 139,063,238 people (42.2% of the U.S. mainland population)

Both Albertsons and Kroger locations: 184,238,217 people (56.0% of the U.S. mainland population)

We also looked at the number of people living within a 15-minute drive of these stores:

Albertsons locations: 124,552,286 people (37.8% of the U.S. mainland population)

Kroger locations: 146,835,469 people (44.6% of the U.S. mainland population)

Both Albertsons and Kroger locations: 192,249,913 people (58.4% of the U.S. mainland population)

These estimates show that a significant portion of the U.S. population lives near an Albertsons or Kroger store and will be impacted by the merger.

What Demographic Groups Are Targeted by the Grocery Chains?

We can use mapping software to see the demographics of people living near Albertsons and Kroger grocery stores. By looking at Consumer Expenditure data, we can estimate how much people spend on groceries within a 1-mile radius of each store.

The analysis shows that, on average, Kroger stores are located in areas where people spend less on groceries than around Albertsons stores. Specifically:

- Kroger locations: Average grocery expenditure is $6,755.46.

- Albertsons locations: Average grocery expenditure is $7,028.07.

- National average: $6,670.54.

This means that Kroger and Albertsons stores are in areas where people spend more on groceries than the national average, but Albertsons stores are in slightly higher-spending areas than Kroger stores.

Understanding the Target Segment of Albertsons and Kroger Stores

Geodemographic Segmentation data helps us understand which types of people Albertsons and Kroger stores are trying to appeal to. Here’s what we’ve found:

Demographic Groups Both Stores Target:

Settled and Content: These are households with moderate to high incomes, where at least one member has gone to college.

Both Albertsons and Kroger aim to serve this group.

- High Earning Families: Similar to Settled and Content, these households have decent to high incomes and members who’ve attended college. Both Albertsons and Kroger stores are popular among these families.

- Bloomers: This group includes households with moderate to high incomes and at least one member who’s been to college. Both Albertsons and Kroger cater to these folks.

Groups Where Albertsons Shines:

- Recent Riches: These are very wealthy households, and Albertsons has a more substantial presence here than Kroger.

- Opulent Homesteads: Similar to Recent Riches, this group comprises affluent households, and Albertsons has a more significant share in this category.

Areas Where Kroger Excels:

- Provincial Lifestyles: These are households in rural areas, and Kroger tends to be more prevalent in these regions than Albertsons.

- Agrarian Outbacks: Like Provincial Lifestyles, these are rural households, and Kroger is the preferred choice.

Understanding the Competition Between Albertsons and Kroger

We closely examined the competition between Albertsons and Kroger across the United States using advanced mapping software. Here’s what we discovered:

Areas of Significant Overlap:

We found that cities like Seattle, Los Angeles, Denver, Dallas, Chicago, and Washington, D.C., have many Albertsons and Kroger stores, which means they compete directly in these regions.

Regional Dominance:

Albertsons tends to dominate in the Northwestern and Northeastern regions of the US, while Kroger is more prevalent in the Southeastern part of the country. This shows their strongholds in different areas.

Proximity to Population:

Our distance radius analysis revealed that most of the US mainland population lives near an Albertsons or Kroger store. About 56.0% of the population is within a 5-mile radius, and 58.4% can reach one of their stores within a 15-minute drive.

Grocery Spending Patterns:

On average, people living near Albertsons locations spend more on groceries than those near Kroger locations. Both Albertsons and Kroger stores have higher-than-average grocery spending, indicating their popularity among shoppers.

Demographic Insights:

People living near Albertsons stores spend more on groceries than those near Kroger stores. Both exceed the national average grocery spending. Albertsons and Kroger attract similar demographic groups, mainly well-educated households with moderate to high incomes. Albertsons stores are often found in areas with very wealthy families, while Kroger stores are more common in rural parts of the US.

Conclusion

The Kroger and Albertsons merger is happening amidst strict enforcement actions and tough talk from the FTC (Federal Trade Commission). The FTC has recently tightened its merger regulations, banned a number of transactions that appeared to be innocuous, and complicated the process even for simple mergers. The heads of the FTC have adopted a wide and controversial stance regarding merger rules. While the FTC’s efforts to change U.S. merger laws might not hold up in court, these actions are making business transactions more costly, which ultimately affects consumers.

The grocery market has changed a lot since the last supermarket merger was challenged in court. Concerns about the merger creating monopsony power (where a company can push down wages or prices it pays suppliers) in labor and supplier markets may be overstated. The retail labor market is competitive, and Kroger and Albertsons have strong unions that negotiate wages. Similarly, the idea that the merged company could unfairly push down prices from suppliers may not hold up, as suppliers would still compete to offer the best deals.